When people talk about artificial intelligence today, the conversation usually revolves around models.

Which company has the smartest system?

Which chatbot performs better?

Which product launches next?

Those questions attract attention. But they may not be the most important questions.

Because underneath the headlines, another competition is happening.

A much quieter competition. A competition measured not in model benchmarks—but in capital.

Who can build?

Who can sustain investment?

Who can absorb mistakes?

Who can survive long enough to monetize?

That competition may ultimately determine the winners.

History suggests something uncomfortable but useful:

Technological revolutions are rarely won by the inventors alone.

They are often won by the organizations that finance infrastructure most effectively.

Railroads changed transportation—but capital allocation determined who survived.

The internet transformed communication—but infrastructure economics separated leaders from casualties.

Cloud computing changed software—but only a handful captured most of the value.

Artificial intelligence appears to be entering a similar phase.

And this time, something unusual is happening.

A small group of technology giants appears willing to commit capital at a scale that resembles industrial expansion more than software development.

The immediate question becomes:

How are they paying for it?

The answer turns out to be one of the most important investor frameworks of this decade.

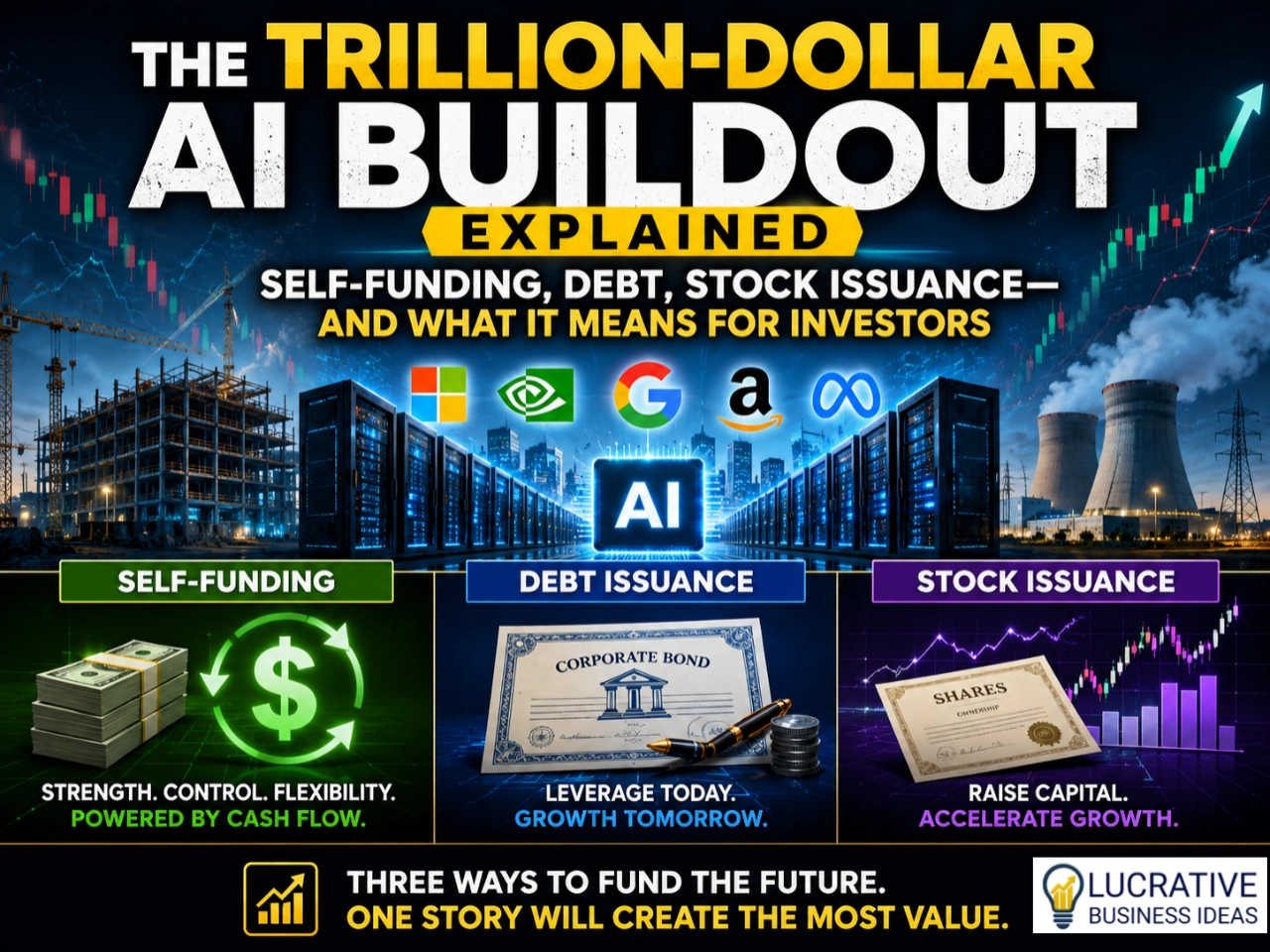

Broadly speaking, there are three major funding models powering the AI buildout:

- Self-funding

- Debt issuance

- Selling more stock

Each sends a different signal. Each carries different risks.

And each may tell us something about where we actually are in the market cycle.

But before understanding the money—we need to understand the cycle.

Part I — Before Following the Money, Understand the Cycle

One of the easiest mistakes investors make during technological revolutions is confusing spending with success.

Large investment feels persuasive. But investment alone proves nothing.

History repeatedly shows that transformational technologies usually go through phases.

Understanding those phases changes how funding decisions should be interpreted.

Every Technology Revolution Begins as an Infrastructure Story

Popular history tends to remember breakthrough products.

Markets remember something else – Who financed the buildout.

Before railroads produced returns, somebody had to lay tracks.

Before electricity transformed industry, somebody had to build generation systems.

Before cloud computing generated enormous cash flows, somebody had to build data centers.

Artificial intelligence appears to be entering the same pattern.

The difference is that this infrastructure wave is being financed largely by corporations rather than governments.

And unlike previous software booms, AI infrastructure is surprisingly physical.

That changes everything.

What Big Tech Is Actually Building

When investors hear:

“Company X plans to spend tens of billions on AI…”

many imagine software.

That mental model misses what is happening.

Much of today’s AI spending is directed toward physical capability.

Infrastructure such as:

- Data centers

- Compute clusters

- Accelerators and specialized hardware

- Networking architecture

- Cooling systems

- Land acquisition

- Fiber infrastructure

- Energy contracts

- Semiconductor supply agreements

This resembles industrial investment more than traditional software expansion.

That distinction matters because industrial buildouts follow different financial rules.

The economics become heavier.

Returns take longer.

Scale advantages become larger.

And financing decisions become more revealing.

The Four Stages of a Technology Market Cycle

Although every cycle looks unique in real time, the broad pattern appears repeatedly.

Understanding these stages provides context for interpreting AI spending.

Stage One: Discovery

A breakthrough becomes visible.

Curiosity dominates.

Most people remain skeptical.

Capital requirements stay relatively low.

Attention exceeds infrastructure.

Stage Two: Land Grab

Competition accelerates.

Companies begin racing for scarce assets.

Investment rises dramatically.

Infrastructure becomes strategic.

Investor enthusiasm expands.

Questions focus on participation.

Stage Three: Monetization

The market begins asking harder questions.

Not: “Can this technology change the world?”

But: “Who captures the economics—Revenue quality, Margins, Returns, Unit economics?”

Execution starts mattering more than narrative.

Stage Four: Consolidation

The strongest survivors emerge.

Infrastructure normalizes.

Competition narrows.

Long-term profitability becomes visible.

Excitement fades.

Economic reality takes over.

Where Are We in the AI Cycle Today?

No one knows with certainty. But markets leave clues.

If we interpret current capital behavior carefully, the evidence appears consistent with this possibility:

We may be transitioning from late-stage infrastructure expansion toward early-stage monetization.

Several observations support this interpretation:

- Leading companies continue investing aggressively.

- Capital remains available.

- But investors are becoming more selective.

- Questions are changing.

- Less focus on model announcements.

- More focus on economics.

- Less focus on experimentation.

- More focus on utilization.

That shift matters. Because financing choices become increasingly meaningful during this transition.

And that brings us to the first—and historically strongest—funding model—Self-funding.

Part II — Self-Funding

Why Internal Capital May Be the Strongest Signal in the AI Race

Before we examine borrowing and stock issuance, we need to begin with the funding model that investors have historically treated with the most respect.

Not because it guarantees success. But because of what it usually signals.

Self-funding.

At first glance, self-funding sounds almost boring.

- A company earns money.

- The company reinvests money.

- End of story.

In practice, it may be one of the most powerful strategic advantages in modern business.

Because when a company finances a technological revolution using profits generated from its existing operations, it reveals something deeper than access to capital.

It reveals confidence. And in some cases, it reveals dominance.

What Self-Funding Actually Means

Self-funding happens when a company finances growth primarily through internally generated capital.

Instead of depending heavily on new debt or issuing additional equity, the business reinvests cash produced by existing operations.

That cash may come from:

- Cloud computing

- Enterprise software

- Advertising

- Platform ecosystems

- Subscription services

- Existing infrastructure businesses

This distinction matters. Because capital raised externally and capital produced internally behave differently.

External capital arrives with obligations. Internal capital arrives with flexibility.

That flexibility can become a major competitive advantage during infrastructure cycles.

Why Self-Funding Has Historically Been Viewed as a Strength Signal

Imagine two companies announcing identical plans.

Each intends to invest $100 billion into AI infrastructure.

The first company says:

“We generated this capital from operations.”

The second says:

“We raised it externally.”

Same spending. Different message.

The market often interprets those messages differently because internally funded investment usually implies three things:

- Existing customers already generate substantial economic value.

- Management has room to think long term.

- The business can absorb uncertainty.

That does not guarantee intelligent decisions. But it changes the probability profile.

Self-funded companies usually have more control over timing, execution, and endurance.

The First Advantage: Ownership Stays More Intact

One of the least appreciated benefits of self-funding is ownership preservation.

When expansion is financed internally, existing shareholders often avoid significant dilution.

This sounds technical. It is not.

Ownership determines who receives future rewards.

Suppose investors collectively own a business today.

If the company repeatedly issues stock later, ownership percentages gradually shrink.

Self-funding reduces pressure to make those tradeoffs.

That does not mean shareholders automatically benefit. Management still has to invest well.

But preserving ownership while creating growth can become extremely powerful over time.

The Second Advantage: Management Gains Strategic Patience

Infrastructure cycles rarely reward impatience.

Returns often arrive later than expected.

Competitors emerge.

Costs fluctuate.

Markets become emotional.

Self-funded companies often gain something difficult to measure: Time.

Management can continue building without immediately returning to lenders or public markets.

That flexibility matters. Because strategic patience frequently separates infrastructure leaders from infrastructure casualties.

The ability to endure uncertainty becomes part of the competitive advantage.

The Third Advantage: Strong Businesses Can Create Reinforcing Loops

This may be the most important idea in this section.

Large technology platforms often operate inside reinforcing systems.

One successful business funds another.

Which strengthens another.

Which expands cash generation.

Which finances further expansion.

The loop can look like this:

Existing business → Cash generation → Infrastructure investment → Improved capability → More customers → Higher cash generation → Additional investment

Once this mechanism begins working at scale, competition becomes harder.

Not impossible. But harder. Because competitors are no longer competing only against products.

They are competing against internal capital engines.

Why Investors Sometimes Overestimate the Safety of Self-Funding

Now we arrive at the uncomfortable part.

Self-funding is respected. But it is not automatically safe.

Large cash generation can create a dangerous illusion.

That illusion sounds like this:

“We can afford mistakes.”

History repeatedly shows otherwise.

Strong balance sheets sometimes encourage overbuilding.

Large companies can become convinced that scale itself guarantees returns.

It does not.

Infrastructure spending can exceed demand.

Costs can arrive before monetization.

Execution can disappoint.

The result is not always failure. Sometimes it simply means years of lower returns.

That distinction matters.

Investors should never confuse financial capacity with capital discipline.

Those are different things.

The Hidden Cost of Self-Funding: Opportunity Cost

Every dollar invested in AI loses the opportunity to do something else.

This creates invisible tradeoffs.

Management constantly chooses between competing priorities.

Should capital be directed toward:

- Dividends?

- Share repurchases?

- Acquisitions?

- New business lines?

- Debt reduction?

- AI infrastructure?

There is no universal answer.

But those choices reveal management’s real priorities.

Investors often learn more from where capital goes than from what executives say.

What Self-Funding May Be Signaling About This Stage of AI

Now connect this back to the market cycle.

Large-scale self-funding often appears after uncertainty begins narrowing.

Not at the earliest experimental stage.

And not after economics are fully proven.

Instead, it tends to appear during a transition.

A period where leaders increasingly believe:

This infrastructure is becoming necessary.

Waiting carries risk.

The opportunity appears large enough to justify aggressive reinvestment.

That interpretation fits many features of today’s AI environment.

Again—that does not guarantee correct decisions. But it helps explain behavior.

The Investor Framework: When Should Self-Funding Be Viewed Positively?

Investors should not reward spending automatically. They should ask better questions.

Self-funding tends to deserve confidence when:

- Core business remains healthy

- Returns remain measurable

- Infrastructure strengthens competitive position

- Cash generation stays durable

- Management remains disciplined

Self-funding deserves caution when:

- Investment becomes symbolic

- Margins deteriorate materially

- Returns become difficult to explain

- Spending outruns business quality

- Growth narratives replace economics

The distinction matters. Because self-funding can either represent strength—or become expensive overconfidence.

Transition: When Internal Capital Is Not Enough

But even the strongest companies eventually face a decision.

Protect internal cash?

Or accelerate expansion?

That is where the second funding model enters—Debt.

Borrowing introduces a completely different logic.

Instead of asking: “What can we afford?”

the question becomes: “What are future returns worth today?”

And that question has shaped some of the greatest—and most painful—expansion cycles in history.

Part III — Debt Issuance

Smart Leverage or the First Warning Sign?

If self-funding is usually interpreted as a signal of internal strength, debt introduces something more complicated.

Leverage.

And leverage has always made investors uncomfortable, for understandable reasons.

Debt can turn a good business into a great one. Debt can also turn a temporary mistake into a permanent problem.

That dual nature is why debt remains one of the most misunderstood tools in markets.

Some investors see borrowing and immediately assume weakness.

Others see borrowing and automatically interpret ambition.

Neither reaction is sophisticated enough.

Debt is neither confidence nor desperation. Debt is an amplifier.

And understanding that distinction may become increasingly important as companies continue financing the AI buildout.

Why Borrow at All If You Already Have Money?

At first glance, borrowing appears unnecessary.

If a company already generates enormous cash flows, why not simply spend existing cash?

This question sounds logical. But large-scale capital allocation rarely works that way.

Professional capital allocation is not about spending available money.

It is about preserving optionality while maximizing expected returns.

That means a company may choose to borrow even when it could technically self-fund.

Why? Because cash itself has strategic value.

Cash provides flexibility.

Liquidity creates resilience.

Preserving capital can sometimes be more valuable than deploying it.

This leads to an important insight:

Companies do not always borrow because they lack money.

Sometimes they borrow because they want to protect choices.

What Debt Issuance Actually Means

Debt issuance simply means raising capital today in exchange for repayment obligations later.

That capital can come from several sources:

- Corporate bonds

- Bank financing

- Long-term credit facilities

- Private capital arrangements

- Convertible structures

The mechanics vary. The principle remains the same.

Future cash flows become partially committed. That changes incentives.

Unlike stock issuance, debt generally does not immediately reduce ownership.

But unlike self-funding, debt introduces obligations that cannot be ignored.

Interest accumulates.

Repayment schedules matter.

Time becomes more important.

Why Debt Has Financed So Many Major Economic Transformations

Debt often appears during periods of infrastructure expansion.

Not because businesses are weak. Because infrastructure frequently requires capital before returns become visible.

History provides countless examples.

- Railroads expanded with financing.

- Telecommunications networks required enormous capital.

- Industrial manufacturing relied heavily on leverage.

- Energy systems expanded through borrowing.

Infrastructure projects rarely wait for full monetization. They build first. Then earn later.

Debt exists partly because of this reality.

It allows organizations to bring future productive capacity into the present.

Used well, this can create extraordinary outcomes.

The Good Version of Debt: Productive Leverage

Debt creates value under one condition:

The return generated by investment exceeds the cost of financing.

That sounds simple. But it explains almost everything.

Healthy leverage often follows this sequence:

Borrow → Build → Grow → Generate cash → Repay → Retain value

When this sequence works, debt becomes a force multiplier.

- Infrastructure arrives faster.

- Scale arrives earlier.

- Competitive positioning improves.

- Shareholders retain ownership.

This is why experienced investors rarely fear leverage by default.

Debt is not automatically risk. Debt can be intelligent acceleration.

Why Debt Changes the Psychology of Decision-Making

The moment obligations enter a business, behavior changes.

Even excellent companies become more sensitive to timing.

Questions become sharper. Execution becomes more important. Because lenders expect repayment whether market conditions cooperate or not.

That pressure creates both benefits and dangers.

Benefits:

- More disciplined investment

- Better capital prioritization

- Faster execution

Risks:

- Reduced flexibility

- Higher operational pressure

- Shorter margin for error

Leverage rewards precision. And infrastructure cycles rarely unfold precisely.

That tension matters.

The Three Warning Signs Investors Should Watch

Debt itself is not the warning signal. The surrounding conditions are.

Warning Sign One: Borrowing Expands Faster Than Economic Visibility

Borrowing ahead of visible demand is not automatically wrong. But uncertainty matters.

Investors should ask:

- What supports repayment?

- Where does future cash generation come from?

- How sensitive are assumptions?

Infrastructure without economics eventually becomes expensive capacity.

Warning Sign Two: Debt Begins Supporting Weakness Instead of Strength

Healthy debt usually supports expansion.

Dangerous debt often compensates for underperformance.

There is an important difference.

If borrowing continues increasing while:

- profitability weakens,

- cash generation slows,

- margins compress,

investors should investigate carefully.

Leverage should enhance strength. Not conceal weakness.

Warning Sign Three: Financing Starts Becoming the Story

This signal is subtle.

Healthy growth companies usually talk about:

- products,

- customers,

- economics,

- execution.

When discussion increasingly shifts toward:

- refinancing,

- liquidity,

- capital access,

- balance-sheet management—

investors should pay attention.

Funding should support strategy. It should not become strategy.

What Debt May Be Signaling About This AI Cycle

Now connect debt back to market behavior.

Debt tends to become more common during transitions.

- Early cycles are funded by possibility.

- Middle cycles require infrastructure.

- Later cycles depend on cash flow.

Borrowing often increases when companies begin believing future economics are becoming more predictable.

That can be healthy. But history adds an important warning.

During major booms, leaders often borrow intelligently.

Followers sometimes imitate aggressively.

Those two situations can look similar in headlines.

But they produce very different outcomes.

One expands advantage.

The other expands exposure.

Investors should learn to distinguish between: borrowing from strength and borrowing from necessity.

That distinction becomes increasingly important as infrastructure spending rises.

The Investor Framework: When Should Debt Be Viewed Positively?

Debt tends to deserve confidence when:

- Cash generation remains strong

- Financing costs remain manageable

- Investment supports durable advantage

- Revenue visibility improves

- Management communicates clearly

Debt deserves caution when:

- Expectations become speculative

- Utilization remains unclear

- Financing complexity increases

- Margin pressure accelerates

- Borrowing becomes habitual

The question is never: “Do they have debt?”

The better question is: “If borrowing stopped tomorrow, would the strategy still make sense?”

That question changes how investors think.

Transition: The Funding Model That Feels Painless

Debt creates pressure.

Self-funding creates opportunity cost.

But the third funding model feels different.

- No repayment.

- No interest.

- No immediate cash stress.

At first glance, it can appear almost painless.

Which is exactly why investors sometimes underestimate it.

Because when companies fund growth by selling more stock—the money arrives immediately.

But ownership quietly changes.

Part IV — Selling More Stock

Growth Fuel or Silent Dilution?

If self-funding represents internal strength…

and debt represents accelerated conviction…

stock issuance represents something else entirely—Flexibility.

- No repayment schedule.

- No interest expense.

- No lender restrictions.

- No immediate pressure.

At first glance, this can look like the safest funding model of all.

And that appearance is exactly why investors sometimes misunderstand it.

Because equity financing rarely sends obvious warning signals.

Debt creates visible obligations.

Self-funding creates visible opportunity costs.

Stock issuance changes something quieter—Ownership.

And ownership changes often happen slowly enough that investors do not notice until years later.

That makes this funding model uniquely powerful—and uniquely easy to misuse.

Why Selling More Stock Feels Different from Borrowing

Debt asks a company to repay money.

Equity asks investors to share ownership.

That difference changes incentives immediately.

When companies issue stock, they raise capital by creating additional shares.

New investors enter.

Existing shareholders remain. But their percentage ownership decreases.

This process is called dilution.

The word itself often sounds negative. But dilution is not automatically bad.

The real question is not whether dilution happens.

The real question is whether dilution purchases something valuable enough to justify it.

The First Big Investor Mistake: Treating Dilution as Automatically Bad

Imagine owning 1% of a company worth $100 billion.

Now imagine management issues shares and your ownership falls to 0.8%.

That sounds worse.

But what if the capital raised helps build a business eventually worth $500 billion?

Your ownership percentage became smaller—

but the value of your stake became larger.

This is why sophisticated investors think differently.

They focus less on percentage ownership alone.

And more on:

value created per share.

That distinction changes everything.

Why Companies Choose Equity Even When Debt Exists

This raises an obvious question.

If debt preserves ownership—why issue stock at all?

Because debt transfers risk back to the company.

Equity spreads risk across investors.

When future economics remain uncertain, equity can become attractive.

Equity effectively says: “We are raising capital without committing future cash flows.”

That flexibility can be valuable during periods of rapid technological change.

Especially when:

- monetization timelines remain uncertain,

- infrastructure needs remain large,

- competitive positioning matters.

Equity allows companies to remain aggressive without becoming financially rigid.

That advantage matters more than many investors realize.

Why Stock Issuance Has Historically Played a Major Role in Innovation Cycles

History shows a recurring pattern.

Many transformative periods relied heavily on equity markets.

Why? Because uncertain opportunities often require patient capital.

Equity gives businesses room to experiment.

- Room to build.

- Room to adapt.

This has appeared repeatedly across market history.

New industries often raise capital before economics fully stabilize.

That does not automatically imply speculation.

It often reflects uncertainty.

Investors who participate accept that uncertainty in exchange for upside.

That exchange can work extremely well—when discipline remains intact.

The Good Version of Stock Issuance: Financing Optionality

The strongest case for issuing equity usually appears under one condition:

Management believes future investment opportunities exceed the cost of ownership dilution.

In simple language:

If markets value the company highly, management may choose to exchange a small portion of ownership for a large increase in capability.

That can be extremely rational.

Imagine this sequence:

Issue limited stock → Raise capital → Build infrastructure → Strengthen economics → Increase future value

When that sequence works, shareholders may become better off despite dilution.

This is one reason experienced investors do not automatically reject stock issuance.

Context matters. Execution matters. Returns matter.

The Hidden Risk: Dilution Rarely Feels Expensive Until It Compounds

Unlike debt, dilution does not arrive with invoices.

That makes it psychologically easier to overuse.

- There is no interest payment.

- No refinancing discussion.

- No lender pressure.

Which means management teams can sometimes issue stock repeatedly without creating immediate discomfort.

But dilution compounds. Slowly. Quietly. Then suddenly.

Over time investors may discover:

Revenue increased. Infrastructure expanded. But ownership became increasingly fragmented.

That realization can surprise investors who focused only on growth.

This is why experienced investors ask:

How much of that future actually belongs to current shareholders?

That question deserves more attention than it usually receives.

What Stock Issuance May Reveal About Management Thinking

Financing decisions often reveal incentives. Not perfectly. But directionally.

Stock issuance may signal several possibilities.

Management may believe:

- future opportunities justify expansion,

- preserving cash matters,

- balance-sheet flexibility is valuable,

- markets are receptive,

- current valuations are attractive.

That last possibility deserves attention.

When companies raise equity during periods of elevated valuations, investors should not automatically interpret that negatively.

Management may simply believe:

“If markets are willing to provide inexpensive capital, we should use it intelligently.”

That logic has created enormous success.

It has also created expensive mistakes.

Execution determines which outcome follows.

What Equity Financing May Be Signaling About This AI Cycle

Now connect this back to the bigger picture.

Equity financing often becomes easier during periods of optimism.

Capital becomes abundant.

Investors become willing to fund future possibilities.

That does not automatically indicate speculative excess.

But it can suggest markets remain confident.

Historically, this often appears during infrastructure expansion phases.

The important distinction becomes:

- Healthy optimism finances value creation.

- Speculative optimism finances narratives.

Those two environments can feel similar—until results arrive.

The Investor Framework: When Should Stock Issuance Be Viewed Positively?

Equity financing tends to deserve confidence when:

- Capital strengthens long-term economics

- Ownership dilution remains disciplined

- Infrastructure creates durable advantage

- Returns improve over time

- Management communicates clearly

Equity deserves caution when:

- Issuance becomes routine

- Capital efficiency weakens

- Share counts rise rapidly

- Growth becomes difficult to monetize

- Financial engineering replaces business quality

The question is never: “Did they issue stock?”

The better question is: “What did shareholders receive?”

- Infrastructure?

- Capability?

- Cash flow?

- Strategic advantage?

- Or simply more spending?

That distinction matters.

Transition: Three Funding Models—Now One Investor Question

At this point, the framework is complete.

We have examined:

- Self-funding.

- Debt issuance.

- Stock issuance.

Three ways to finance the same destination.

But funding decisions are only useful if they help answer a larger question.

- Which model deserves the most confidence?

- Which creates the most risk?

- And what do these choices collectively reveal about where we actually are in the AI market cycle?

That is where we go next.

Because ultimately—the story was never just about artificial intelligence.

It was always about capital allocation.

Part V — The Investor Verdict

Which Funding Model Wins, What It Means for Investors, and Where the AI Cycle May Go From Here

At this point, the framework is complete.

We began with the market cycle.

Then we examined the three major ways companies finance large technological transitions:

- Self-funding.

- Debt issuance.

- Selling more stock.

Now we arrive at the question investors actually care about.

Not: “How are they raising money?”

But: “What does the funding method reveal about future outcomes?”

Because eventually every infrastructure boom reaches the same moment.

The excitement becomes normal.

The headlines become repetitive.

The spending becomes expected.

And markets begin asking harder questions.

- Who created value?

- Who only created activity?

- Who built an advantage?

- Who simply built expenses?

That is where funding decisions become more important than spending announcements.

The First Rule: Spending Is Not Evidence of Success

One of the easiest traps during technological revolutions is assuming that large spending automatically signals leadership.

History repeatedly warns against this.

Large spending can create dominance. Large spending can also create extraordinary waste. The amount invested tells us very little on its own.

What matters is: How efficiently capital becomes economic output.

That distinction separates infrastructure from empire-building.

Markets eventually reward returns. Not announcements.

If We Ranked the Three Funding Models, What Comes First?

This ranking assumes one objective:

- Long-term shareholder value creation.

- Not media attention.

- Not quarterly excitement.

- Not narrative momentum.

- Pure long-term economics.

First Place: Self-Funding

Usually the strongest long-term signal

If forced to choose one funding model that historically deserves the greatest respect, this would usually be it.

Self-funding tends to create the strongest alignment.

- The company earns.

- The company reinvests.

- Existing ownership remains more intact.

- Management retains flexibility.

- Execution determines results.

This model often works best when:

- cash generation is durable,

- infrastructure supports long-term advantage,

- capital discipline remains visible.

But investors should avoid romanticizing it.

Strong companies sometimes become overconfident.

Large internal cash generation can encourage overbuilding.

That is why the best self-funded businesses combine ambition with restraint.

Second Place: Debt Issuance

Potentially powerful—but demands precision

Debt occupies second position.

Used intelligently, leverage can accelerate growth without immediately reducing ownership.

This is why experienced investors rarely fear debt by default.

Debt often works well when:

- economics appear increasingly visible,

- returns are expected to exceed financing costs,

- management remains disciplined.

But leverage changes behavior.

- Once obligations exist, flexibility declines.

- The margin for error narrows.

- Debt magnifies outcomes.

- Strong execution becomes stronger.

- Weak execution becomes painful.

Debt is rarely dangerous because it exists.

Debt becomes dangerous when confidence outruns reality.

Third Place: Selling More Stock

The most flexible—and often the easiest to misuse

This ranking surprises people.

Why place stock issuance third if it creates no repayment pressure?

Because dilution often hides consequences.

Investors feel debt.

They frequently underestimate ownership erosion.

That does not make equity bad.

Many extraordinary businesses used stock intelligently.

But equity becomes concerning when growth depends more on market enthusiasm than business strength.

Over time, ownership changes matter.

And investors who ignore that often discover the consequences later than they expect.

The Framework That Explains Everything: Match Funding to Certainty

This may be the most useful framework in the entire article.

Funding methods tend to align with levels of confidence.

High Certainty → More Self-Funding

When economics appear increasingly visible, internally generated capital often becomes attractive.

Moderate Certainty → More Debt

When returns appear likely but timing remains uncertain, borrowing can accelerate growth.

Lower Certainty → More Equity

When outcomes remain difficult to predict, sharing risk with shareholders can make sense.

This framework is not universal.

But it often explains capital behavior surprisingly well.

And that makes funding choices more revealing than many investors realize.

So What Does Big Tech’s Behavior Suggest Right Now?

Now we return to the original question.

What does all this tell us about where we may be in the AI market cycle?

No one knows with certainty. But capital leaves footprints.

Several observations appear worth paying attention to.

Signal One: AI Is Increasingly Being Treated Like Infrastructure

Leading companies appear to be investing as if AI is becoming a foundational operating layer.

Not an experiment. Not a side project.

Infrastructure spending tends to increase when management believes delay creates strategic risk.

That is meaningful.

Signal Two: Markets Still Believe Future Economics Will Arrive

Capital remains available. Large commitments continue. Investors still appear willing to support expansion.

But optimism increasingly comes with conditions.

Markets are becoming more selective.

That transition matters.

Signal Three: The Narrative Phase May Be Maturing

Earlier phases rewarded association.

Now investors increasingly want evidence.

Questions are becoming operational.

- Revenue.

- Utilization.

- Returns.

- Margins.

That shift often appears when markets begin moving from excitement toward accountability.

The Five Questions Investors Should Ask Before Getting Excited About AI Spending

If you remember only one section from this article, make it this.

Whenever a company announces major AI investment, ask:

1. Where is the capital coming from?

Internal cash?

Borrowing?

Equity?

2. What existing economic engine supports this investment?

Advertising?

Cloud?

Software?

Something else?

3. What evidence exists that demand is real?

Usage?

Customers?

Pricing power?

Retention?

4. How long before returns must appear?

Short-term?

Medium-term?

Long-term?

5. If expectations disappoint, who absorbs the downside?

Shareholders?

Lenders?

Management?

Employees?

Those questions often reveal more than the announcement itself.

My Interpretation of This Moment

If I had to summarize this phase in one sentence, it would be this:

The AI buildout looks less like a traditional software cycle and more like a modern infrastructure cycle.

That does not guarantee extraordinary returns.

And it does not guarantee disappointment.

It simply means investors should think differently.

The winners may not be:

- the biggest spenders,

- the loudest companies,

- or the fastest movers.

They may be the businesses that combine:

- financial strength,

- capital discipline,

- execution quality,

- and patient monetization.

History has rewarded those combinations repeatedly.

See Also:

- 50 Jobs AI May Replace & 50 Jobs That Are Safest from Artificial Intelligence

- All About First Principle Thinking & Other Powerful Problem-Solving Frameworks Used By Entrepreneurs & Other Successful People

Final Conclusion: The Winners May Be Decided by Capital Allocation More Than AI Itself

Artificial intelligence may become one of the defining technologies of this century.

But technology alone rarely determines outcomes. Capital allocation does.

Every company participating in this buildout is making a bet.

Some are writing checks from operating profits.

Some are borrowing against future expectations.

Some are exchanging ownership for acceleration.

Years from now, investors may look back and realize something important.

The signals were visible all along.

Not hidden in product launches.

Not hidden in model rankings.

But hidden in financing decisions.

Because markets eventually ask every company the same question:

You built something impressive. Now show us the economics.

Frequently Asked Questions (FAQs) About The Three Ways Big Tech Is Funding the Trillion-Dollar AI Buildout

1. Why are Big Tech companies spending so aggressively on AI right now?

Because large technology shifts often create periods where waiting becomes more expensive than acting.

From the outside, today’s AI spending can appear excessive.

But infrastructure cycles rarely look rational in real time.

When railroads expanded, many observers thought spending was excessive.

When cloud computing infrastructure accelerated, similar concerns appeared.

Artificial intelligence may be creating a comparable environment.

Large technology companies are not only competing to launch products.

They are competing to secure infrastructure advantages.

That includes:

- Compute capacity

- Data center availability

- Energy access

- Hardware supply

- Engineering talent

- Platform positioning

Management teams may believe that building too early carries risk—but building too late carries even greater risk.

That does not guarantee current spending levels will produce attractive returns.

But it helps explain why spending continues even while investors ask tougher questions.

2. Is the current AI buildout a bubble?

The honest answer is: No one knows with certainty.

But the more useful question may be: What kind of bubble are we talking about?

There are at least two possibilities.

Scenario One: Infrastructure investment becomes larger than near-term demand.

That can temporarily reduce returns.

Scenario Two: Infrastructure ultimately proves justified—but expectations arrive too early.

History contains examples of both.

The internet experienced enormous overinvestment in some areas while still changing the world.

Cloud infrastructure looked expensive before becoming highly profitable.

Technology revolutions often combine real innovation with periods of capital excess.

That means investors should avoid extreme conclusions.

Not every boom becomes collapse.

Not every breakthrough produces immediate profits.

3. Why is self-funding usually considered the strongest financing model?

Because self-funding typically signals that a business already generates enough economic value to finance expansion internally.

That creates several advantages.

- First, ownership is often preserved.

- Second, management gains flexibility.

- Third, the business becomes less dependent on external market conditions.

But self-funding is not automatically superior.

A company can generate enormous cash flows and still invest poorly.

Investors should focus less on the funding source itself and more on whether investment improves long-term economics.

Strong funding does not replace disciplined execution.

4. If debt adds risk, why do smart companies still borrow?

Because debt can improve capital efficiency.

Borrowing is not always a sign of weakness.

Sometimes management deliberately chooses leverage because preserving internal liquidity creates more strategic flexibility.

Debt becomes attractive when:

- future returns appear reasonably visible,

- financing costs remain manageable,

- investment opportunities look compelling.

The danger appears when borrowing becomes a substitute for business quality.

Good debt accelerates success.

Bad debt postpones reality.

That distinction matters.

5. Is selling more stock always bad for investors?

No. This is one of the most misunderstood ideas in investing.

Many investors immediately react negatively to dilution.

But dilution itself is not automatically destructive.

If issuing stock allows a company to create substantially more value than ownership lost, shareholders may still benefit.

The better question is: Did management convert dilution into durable economic improvement?

If the answer is yes, stock issuance may have been intelligent.

If not, dilution becomes expensive.

6. Which funding model should investors generally prefer?

If all other conditions are equal:

Self-funding is usually the strongest signal.

Debt often comes second.

Stock issuance generally ranks third.

But this ranking depends heavily on context.

A poorly executed self-funded strategy can underperform.

A well-structured debt strategy can outperform.

A disciplined equity strategy can create extraordinary value.

Investors should avoid turning financing methods into ideology.

Capital structure should fit business reality.

7. What is the biggest mistake investors make during infrastructure booms?

Confusing activity with value creation.

Large spending creates excitement. Excitement attracts attention. Attention creates narratives.

But none of those automatically create returns.

Investors often assume:

- Big investment = market leadership.

History repeatedly shows otherwise.

Better questions include:

- What returns are being generated?

- How durable are those returns?

- How quickly can investment be monetized?

- What assumptions must become true?

Those questions usually matter more than spending totals.

8. How can ordinary investors evaluate AI spending without reading financial statements all day?

Start with five simple questions.

- Question One: Where is the money coming from?

- Question Two: What existing business supports the investment?

- Question Three: What evidence suggests demand exists?

- Question Four: How long before returns appear?

- Question Five: Who absorbs downside risk?

You do not need institutional tools to think clearly.

You need disciplined questions.

That alone filters out a surprising amount of noise.

9. Could smaller companies eventually outperform the biggest AI spenders?

Absolutely. History repeatedly shows that infrastructure builders and value creators are not always identical.

Large companies often win infrastructure phases.

Smaller companies sometimes win application layers.

Some businesses become utilities.

Others become category leaders.

Others become acquisition targets.

The existence of dominant infrastructure does not eliminate opportunities elsewhere.

It changes where opportunities emerge.

Investors should remain open to multiple winners.

10. What single lesson should readers remember from this entire article?

Remember this:

Technology changes industries. Capital allocation determines outcomes.

Artificial intelligence may become one of the most important technological transitions of this century.

But the companies that ultimately win may not simply be the smartest.

They may be the organizations that combine:

- financial strength,

- disciplined investment,

- operational execution, and

- patient monetization.

Because markets eventually stop rewarding ambition alone.

They begin rewarding economics.

And when that transition happens, financing decisions often become more revealing than product announcements.